Food and farming are back in the headlines as prices spiral following the invasion of Ukraine, providing a reminder that the food we eat is fundamental to all human society. This can be a surprising notion for tech-enabled urbanites in developed countries but, as in the Arab Spring a decade ago, we are again seeing that food retains the power to influence economics and geopolitics.

Prior to the war in Ukraine, Russia and Ukraine together accounted for 30% of the world’s wheat exports and 60% of sunflower oil exports. Both are widely used in food for animals and humans alike, and are difficult to replace. In addition, one-third of the world’s potash, used for fertiliser, comes from Russia and Belarus, neither of which can export it under current sanctions, while China, another significant exporter of fertiliser, implemented an export ban last year to safeguard its own supplies. Again, potash supplies are not easily replaced, and the shortage will have an impact across the food chain – from cereal farming to animal feeds and high-value crops, such as fruits and vegetables.

As we have written elsewhere, this triple constraint on grain, vegetable oils and fertilisers is likely to presage tragedy for many people in developing economies, where expenditure on food is a high proportion of overall spending. Suffice to say here that food inflation, climate change and COVID-19 are intensifying a long-running global hunger crisis. Since 2019, the UN Food & Agriculture Organisation’s Food Price Index has risen by 58% to an all-time high, and prices of wheat and maize have doubled.

Today’s food shortages are also a timely reminder, given the apocalyptic warnings contained in the IPCC’s most recent Climate Report published in February. The challenges posed by current supply constraints may prove to be a very light warm-up act for the vast changes that we must make in order to decarbonise agriculture (which accounts for up to one-third of all C02 emissions) and feed a growing population while adapting to climate change.

Sustainable trends in the future of food

These are by no means new issues: the question of how agriculture can adapt to climate change was one of the central themes behind the launch of Sarasin’s Food and Agriculture strategy in 2008, alongside other themes that we believe will dominate how we produce and consume food.

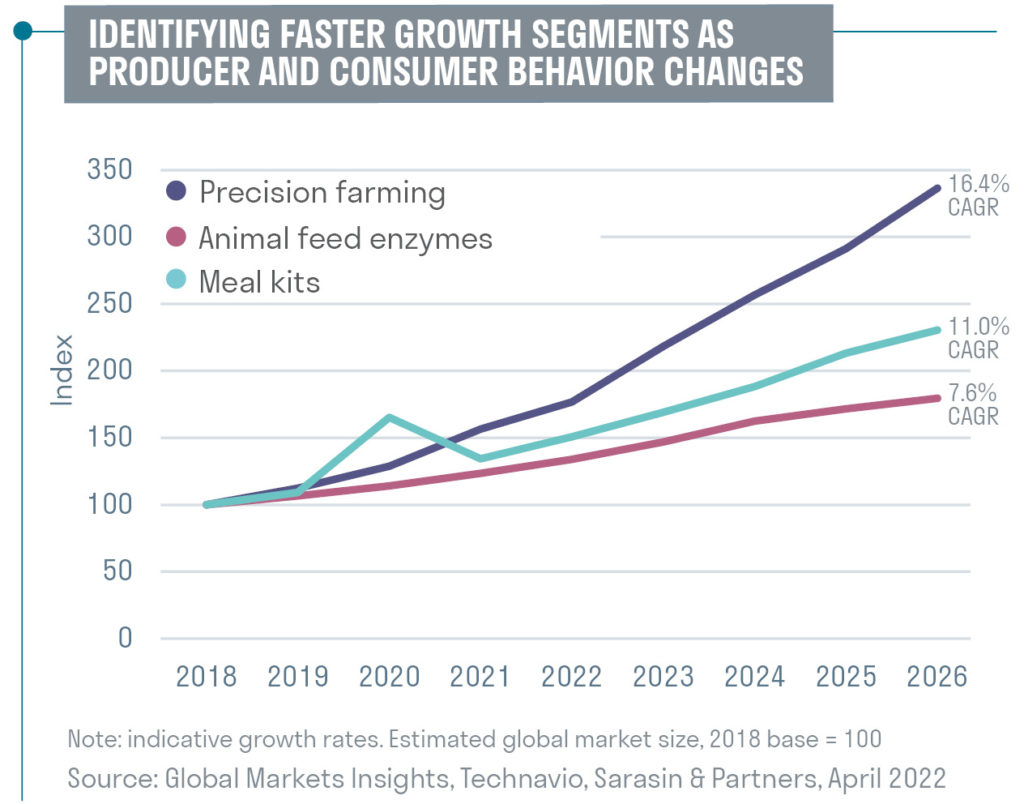

The strategy has a wide remit, with freedom and flexibility to seek out responsible investment ideas across the food spectrum, in areas such as fertilisers and other inputs, food production and logistics, processing, packaging and consumption. These non-cyclical, enduring themes include farming technology (agtech), decarbonisation and changing consumer behaviour, which in turn contain an array of investment sub-themes, such animal feed enzymes, meal kits, precision farming and healthy eating.

Underlying these themes is a shift towards more sustainable and environmentally considerate approaches to food, which is strongly reflected in our strategy’s ESG policy: since launch, the strategy’s portfolios have avoided exposure to pesticides, palm oil and beef producers.

Taking a responsible thematic investment approach can mean forgoing short-term gains. For example, we could have profited handsomely recently from investing in pesticide companies, but we did not. This is because we think that widespread spraying of chemical pesticides is environmentally unsustainable and that technologies such as Deere’s See and Spray system will radically reduce demand for pesticides.

The strategy’s performance has recently had a fallow period, as it has at other times, when our long-term investment themes have not chimed with market fashions. The dominance of the US stocks in equity markets – and of US large-cap consumer tech stocks in particular – followed by a revival of interest in cyclical stocks such as energy companies, miners and banks has kept the spotlight firmly away from the longer-term growth potential that we focus on.

However, the companies that we hold in the strategy have continued to prosper and grow their earnings. As global economic activity begins to slow, long-term investment themes are likely to prove their mettle by continuing to provide steady, long-term annual compound growth rates and welcome diversification away from more mainstream investments.

Old MacDonald had a robot

Agriculture is undergoing its greatest transformation since the Green Revolution of the 1970s as farmers embrace digitisation and smart farm equipment that can provide greater efficiency and productivity gains. Farming has lagged behind other industries in applying new technology, so there is vast growth potential in this area. In addition, we expect the automation and digitisation of farming to accelerate as agriculture decarbonises and farmers seek ways to expand productivity while adjusting to climate change.

As farmers become ‘wired’ they are able to see how their operations are working in real time and therefore make better decisions. One of our favourite agtech companies is market-leader John Deere, which is bringing to farming a number of automation and digital technologies that have been tried and tested in other industries, such as warehousing and logistics.

For example, Deere’s See and Spray equipment uses machine vision to distinguish between weeds and crops and uses precise, directed nozzles to apply weed killer. Deere’s analysis suggests that this technique can result in 75% less herbicide coming into contact with the soil, thus benefitting the environment and reducing farmer’s input costs.

Food bytes

The digitalisation of food delivery was a well-established trend before the pandemic. Lockdowns accelerated this trend, creating a spike in the number of people discovering the benefits of meal kits provided by companies such as Hello Fresh and Gusto.

Another of our long-term digitalisation theme holdings is Ocado. Although people are most familiar with Ocado’s delivery vans and drivers, the company is in essence an automation and robotics company that sells its products and services to large supermarkets around the world. Ocado is making great strides in implementing next-generation warehouse technology, such as roving product-picking robots that are made using 3-D printed parts that can be reproduced and replaced on site.

Ocado’s long-term ambition is to develop highly automated delivery systems that reduce the cost of last-mile delivery to around 10% of the total cost of sales, at which point groceries delivery could be cheaper than a trip to the supermarket.

Profits from protein

The production of proteins, particularly through raising livestock, is a major contributor to greenhouse gas emissions. For this reason, the strategy is positioned towards ‘good’ protein production, such as aquaculture, which has a smaller carbon footprint than livestock.

We are currently focused on healthy eating in conventional foods – such as salmon - rather than in alternative protein names such as Beyond Meat and Impossible Foods. Although the salmon price fluctuates with seasonal supply, its overall trend is upwards as a result of increasing demand from health-conscious consumers, coupled with limited supply; there are only two areas in the world where the conditions are right to farm salmon.

By contrast, barriers to entry in the alternative proteins market are relatively low, and market penetration has been slower than expected. Despite having first mover advantage, access to consumers via fast food restaurants and supermarkets and, in the case of Beyond Meat, a link-up with McDonald’s, both companies have struggled to build on their early success, raising questions about pricing and the size of their potential markets.

We have therefore chosen to adopt a lower-risk exposure to alternative foods via companies such as IFF and DSM, whose products are used to enhance flavours and textures. The expertise and intellectual property that these companies have accumulated are protected by high barriers to entry.

Learning to live and invest with food inflation

The disruption caused by the war in Ukraine is likely to be significant and long-lasting. This will keep food prices higher because it will not be easy to replace the crops and fertilisers these countries usually export. Even if a ceasefire is reached, damage to Ukraine’s railway and port infrastructure means that exports of bulk commodities will be significantly reduced, possibly for years to come.

Cascading impacts along the supply chain and wild cards such as extreme weather may also support inflation. For example, fertiliser use is likely to decline in the coming months as farmers try to cut costs. This will reduce agricultural yields next season, keeping crop prices elevated over the medium term. The impact of higher inflation on consumer demand is more difficult to judge: higher food prices tend to have a limited impact on volumes of food sold, but customers often swap to cheaper options.

We are therefore interested in responsible companies that can pass inflation on to their customers rather than reduce their profit margins. Fortunately, the essential nature of food means that there are a number of inflation plays available in food and agriculture that can provide useful diversifiers for investors seeking to broaden their pro-inflation exposure. Higher prices for essential crops will increase the incomes of farmers who can pass their increased input costs on to consumers. We believe that higher profits for grain and corn farmers will increase the amount they are willing to invest in better farming equipment. We have therefore increased exposure to agtech and fertiliser companies, both of which will benefit from higher food prices.

Looking more broadly, the investment ideas available to us for the Sarasin Food and Agriculture strategy are becoming richer and more diverse as food-related companies increasingly tap the public markets for capital. We are particularly excited by the potential in areas such as food protein production, responsible food packaging, biofertilisers and vertical farming.

The production and consumption of food is complex, touching many different aspects of the natural environment and human society. Finding solutions that address supply pressures, changes in consumer preferences and the challenges of climate change opens up a wide range of investment sub-themes that we can expect to endure for many years to come.

Important information

If you are a private investor, you should not act or rely on this document but should contact your professional advisor.

This communication is sent on a confidential basis, and you are welcome to discuss the materials with our staff. This information may not be circulated to others without our permission.

The information on which the document is based has been obtained from sources that we believe to be reliable, and in good faith, but we have not independently verified such information and no representation or warranty, express or implied, is made as to their accuracy. All expressions of opinion are subject to change without notice.

US Persons are able to invest in units or shares of Sarasin & Partners LLP funds if they hold qualified investor status and enter into a fully discretionary investment management agreement with Sarasin Asset Management Limited. US persons are U.S. taxpayers, nationals, citizens or persons resident in the US or partnerships or corporations organized under the laws of the US or any state, territory or possession thereof.

This document has been prepared by Sarasin & Partners LLP (“S&P”), a limited liability partnership registered in England and Wales with registered number OC329859, authorised and regulated by the UK Financial Conduct Authority and approved by Sarasin Asset Management Limited (“SAM”), a limited liability company registered in England and Wales with company registration number 01497670, which is authorised and regulated by the UK Financial Conduct Authority and registered as an investment adviser in the US.

Please note that the prices of shares and the income from them can fall as well as rise and you may not get back the amount originally invested. This can be as a result of market movements and also of variations in the exchange rates between currencies. Past performance is not a guide to future returns and may not be repeated. Management fees and expenses are described in SAM’s Form ADV, which is available upon request or at the SEC's public disclosure website, https://www.adviserinfo. sec.gov/Firm/115788. For your protection, telephone calls may be recorded. SAM and/ or any other member of Bank J. Safra Sarasin Ltd. accepts no liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of his or her own judgment. SAM and/or any person connected to it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

©2022 Sarasin Asset Management Limited – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin Asset Management Ltd.