Outlier events can upend models and instantaneously trigger new inflection points. Oil price shocks, asset price bubbles and monetary policy tightening have historically been the events triggering economic recessions.

Low probability but high impact events, like a pandemic, were not on the typical risk monitor. Yet, the health and economic calamity caused by the pandemic will continue to reverberate for years to come.

HOW CAN WE START TO ASSESS THE DAMAGE AND THE LIKELY PATH FORWARD?

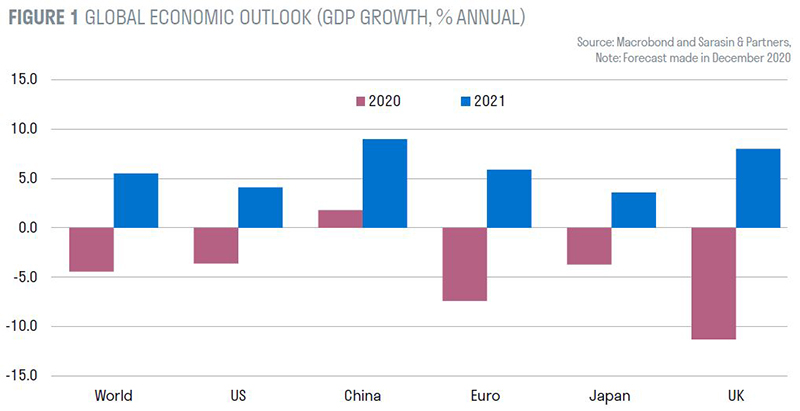

As a starting point, the damage is severe and tragically the human and economics costs continue to mount. The global economy is likely to have contracted by 4.4% annually in 2020 (Real GDP, in USD terms). By magnitude, that’s more than double the fall seen during the global financial crisis in 2009 (-1.7%). By region, the differences are stark.

China, which implemented the most severe restrictions, managed to supress the virus in a relatively short span of time. We forecast the Chinese economy grew by 2% in 2020 – the only major economy to post any economic growth. Large advanced economies, like the US and Japan, are likely to see their economies shrink by around 4%. In the euro area, which is grappling with a further surge of infections and the prospect of a double-dip recession, the contraction is likely to be 7.5%. In the UK, where Brexit uncertainty has compounded the pandemic-related economic costs, the total economic contraction will be higher still, at more than 11%.

THE ROAD AHEAD

The vaccine provides a bright ray of hope and largely underpins our positive economic outlook for 2021.

Crucially, it provides visibility for firms to make business investment decisions, and consumers with confidence to reduce high precautionary savings. Notwithstanding the logistical challenges for successful distribution, we expect the most vulnerable parts of society to be inoculated by the end of Q1 2021 in advanced economies, before the pace of vaccination accelerates to cover 75% of the total population by Q3 2021 – sufficient for herd immunity. As health outcomes improve, government restrictions will start to be rolled back from spring.

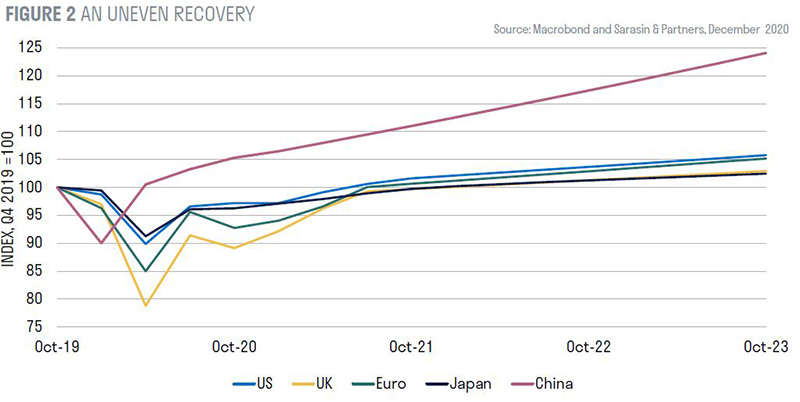

The mechanical re-starting of economic activity will see economic growth rates surge from Q2. But in comparison to the low base of 2020, this will generate statistical illusions that need to be carefully interpreted. The global economy is likely to record annual growth of 5.5% in 2021 – the fastest pace since the oil price shocks of the 1970s. However, this growth will reflect the fact that as much as 30% of the economy was forced to close during the height of the pandemic, rather than structural growth. Given the varying starting positions of countries, the time to fully regain lost economic ground will vary. The recovery will be uneven.

We expect the US economy, fuelled by fiscal-stimulus, will return to its pre-crisis size by Q3 2021, followed by the euro area and Japan towards the end of 2021, and the UK around a year later. So on average, countries will take 2-3 years to heal, while China completed this process in a single quarter.

REGAINING LOST GROUND

Little discussed, but paramount to the economic outlook, is the permanent loss the pandemic will leave once mobility restrictions are withdrawn and a new normality gained. Permanent loss could amount to as much as 5% for some countries unable to catch-up to their pre-crisis GDP trajectory. There’s also the issue of scarring or damage to long-term growth, caused by higher unemployment, destruction of firm-specific capital, weak investment, and a fall in the accumulation of human capital via education.1

Policy makers in Europe have been particularly cognisant of the risk of long term unemployment, by subsidising workers’ pay in short-time work and furlough schemes. At the height of the pandemic, these schemes covered up to a third of the total workforce in Germany, UK, France, Italy and Spain, providing 60-80% of original income.

Yet, the full economic costs will only be seen when the fiscal policy band-aids are pulled off and we can examine the number and type of jobs left standing.

In the US, where policy didn’t try to protect jobs but rather protect household incomes with stimulus cheques, 10 million jobs have still not returned since the pre-crisis peak in February 2019. Similarly, in Europe unemployment rates are likely to surge when the job retentions schemes finally end. Europe faces the additional risk, however, that while job protection schemes are helpful in the short-term, they may prevent the necessary readjustment of the labour market and exacerbate long term structural issues, such as the inevitable decline of some industries and rise of others. This mismatch between the skills required and the skillset available takes time to unwind. Long-term unemployment was a chronic issue in Europe before the pandemic struck. According to the OECD at the end of 2019 the share of unemployed that had been long-term unemployed (defined as over 52 weeks) was 57% in Italy and 39% in France, compared to 12% in the US.

A NEW ERA FOR DEBT?

Another legacy of the crisis could be the general acceptance of high debt levels. The need for nimble policymaking saw fiscal prudence quickly give way to fiscal splurge as governments spent on health, income support, business support, and implemented various tax cuts. According to the IMF2, government budgets surged by an average of 9% of GDP in 2020, and public debt reached 100% of GDP – even higher in advanced economies. This will be a far cry from the 60% debt-GDP threshold that was enshrined in orthodox economic thinking previously.

Given the synchronised rise in public debt across countries, the prospect of low for longer interest rates, and a paradigm shift to question the merits of fiscal consolidation in a low-growth environment, we are unlikely to see an immediate return to the previous days of austerity. Although fiscal sustainability concerns will not disappear, and fiscal discipline and credibility will remain important, sovereign risk is likely to be assessed more broadly than benchmarked against simple debt thresholds. If spent wisely, it could provide governments opportunity to boost chronically low productivity growth.

THE NEW NORMAL

Uneven recoveries, higher unemployment, and higher debt are trends that will likely shape the new normal. Optimists suggest the pandemic has also provided the catalyst for enduring change by reorganising the production process. But early academic evidence from the Bank of England3 suggests that productivity enhancements from creative destruction – whereby low productivity sectors and firms are replaced by high productivity ones - have thus far been limited and insufficient to offset the destruction caused. As for the study of the long-term social impacts, ranging from income and wealth inequality to intergenerational and gender imbalances - the research has only just begun.

1 Source: The lasting scars of the Covid-19 crisis: Channels and impacts, Jonathan Portes – June 2020

2 Source: World Economic Outlook, October 2020: A Long and Difficult Ascent, The IMF – October 2020

3 Source: The impact of Covid-19 on productivity, Bank of England (Staff Working Paper) - December 2020