Key points:

- Bonds have long been the bedrock of balanced investment portfolios: offering real returns and a negative correlation to equities – but can we take that for granted?

- The period of 2000-2020 is etched in the memory of investors: This ‘golden age’ was an unusually favourable period for bonds; history paints a more nuanced picture.

- Resilience demands fresh thinking: More recently bonds have had a wobble. This is not just about a single year (2022), but rather a broader regime shift. At Sarasin, we're challenging assumptions and adjusting – diversifying alongside bonds to build portfolios fit for today's uncertainty.

It has been a rollercoaster ride for government bonds recently. Once the dependable backbone of a balanced investment portfolio, their credentials have been seriously tested. Are bonds still a safe haven? Can they still smooth the bumps when equity markets wobble? These are fair questions, especially after recent events have turned some long-standing assumptions upside down. Let’s take a closer look at what has changed – and what we have learned.

Bonds: Once the great diversifier

Many seasoned investors will confidently say that “government bonds and shares are negatively correlated”. This means that when equities rise, bonds fall, and vice versa. At least that is the conventional wisdom.

Of course, if that relationship of negative correlations holds, that is a very powerful tool for a multi-asset investor. The investment journey is automatically ‘smoother’, as the ups and downs in a portfolio’s equities and bonds offset one another to some degree.

But is this conventional wisdom really true? And does it still hold today? Let’s test this, through the lens of a few market regimes.

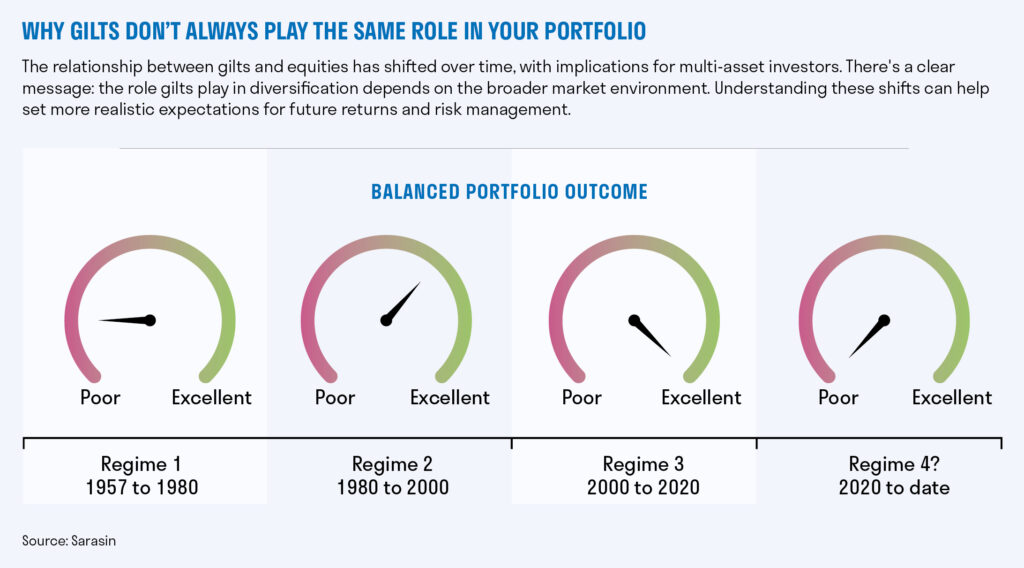

First, let’s take a journey back to the 1960s and 1970s. Let’s call this Regime #1. In that period the relationship between the equities and bonds was, well, pretty neutral. In other words, when equities went up, it was a toss-up whether bonds went up or down. It would be fair to say that in terms of a portfolio diversifier back then, bonds did not really help much. More to the point, they delivered lower returns than cash in that 20-year period, as a result of high inflation[i]. With hindsight we can say cash would have been the better companion to equities in a classic 60/40 (60% equities, 40% bonds) balanced portfolio.

Enter the 1980s. From 1980 right through to the turn of the millennium (Regime #2), bonds and equities became positively correlated. In other words, when equities delivered negative returns, more often than not, so did bonds. Not a great combination, you might say. But why? We think the market was still somewhat scarred from the negative bond returns from the prior decade. In short, it took time for trust in bonds to be regained, even if bonds delivered decent returns in this regime. It is fair to say balanced portfolio investors had a mixed experience.

The millennium turned, and with it the fortunes of bonds turned. This is Regime #3. From 2000 to 2020 bonds really came into their own. In what we can now say was a ‘golden age’ for bonds, they reliably zigged when equities zagged. Even better, bonds delivered handsome total returns too, as inflation and interest rates ground lower[ii]. Many investors built portfolios (and their careers) around this dependable dynamic; they simply knew that when equities fell bonds would come to the rescue. This became something of a recognised truth.

This is why what has happened more recently has been such a shock.

In the illustration above, we look at the average correlations for global equities and UK Gilts. We measure correlations using a rolling one-year window of weekly returns, simulating the total returns of UK gilts prior to 1990.

What’s changed since 2020?

The Covid pandemic was the first big test. As markets panicked in early 2020, bonds initially did their usual job – rallying as equities slumped. That comforting negative correlation was still there, boosted by low inflation and generous central bank support.

Then inflation came knocking – hard. Energy prices soared, supply chains got tangled, and prices across the board shot up. In the UK, inflation peaked north of 10%[iii]. The Bank of England, along with other central banks, responded by aggressively hiking interest rates. In just over a year, UK interest rates jumped from 0.1% to 5.25%[vi].

The result? Bonds and shares fell together. Rising bond yields (which means falling prices) put pressure on both asset classes. Suddenly, that tried-and-tested ‘60/40’ portfolio mix didn’t feel so balanced anymore.

But was this not just a one off reset in 2022, before “normal service” resumes? Sadly not.

Of course, we have had a few brief spells since 2022 where bonds have looked useful again as diversifiers – especially when inflation expectations have cooled – but by and large, that classic diversification benefit has been missing in action.

Fast forward to 2025, and we have seen yet more volatility – this time sparked by US politics. Again, any diversification benefit from bonds was short-lived. It was not long before, worries about inflation and fiscal discipline sent yields soaring and with it bond returns tumbling.

How we’re navigating volatility at Sarasin

Naturally, this analysis is an oversimplification of many things, and misses much nuance. But in short, at Sarasin, we are adjusting how we manage risk.

For example, earlier this year, we reduced our exposure to equities, ahead of the worst of the market falls. However, instead of piling into bonds (as the conventional wisdom says) we chose to diversify into gold and cash. Why? Because while bonds still have a role, we are being pickier than ever.

We’re not saying bonds are obsolete. Far from it. But we do need to rethink how and when they work best. They are not always the perfect diversifier. They are not always negatively linked to equities. And they do not always offer shelter in a storm.

Remaining resilient

If the past few years have taught us anything, it is that we cannot take the old bond rules for granted. In fact, the "old rules” relate only to a relatively short period of time. We were treated to a golden 20-year period with bonds delivering positive real returns, excess returns versus cash, and a negative correlation to equities. With hindsight we can say markets have been spoilt, and investors got used to it.

But the world has changed, and so have markets. In response, we need to be more thoughtful, more selective, and maybe a bit more sceptical about some of the assumptions of the last 20 years. Looking further back in history – as we have done in this article – may well offer a useful guide.

It is only by questioning these long-held beliefs that we can build truly resilient, well-diversified portfolios for our clients.

[i] https://www.federalreservehistory.org/essays/great-inflation

[ii] https://www.federalreservehistory.org/essays/great-recession-and-its-aftermath

[iii] https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/october2022

[vi] https://www.bankofengland.co.uk/boeapps/database/Bank-Rate.asp

Important information

This document is intended for retail investors and/or private clients in the US only. You should not act or rely on this document but should contact your professional adviser.

This document has been prepared by Sarasin & Partners LLP (“S&P”), a limited liability partnership registered in England and Wales with registered number OC329859, which is authorised and regulated by the UK Financial Conduct Authority with firm reference number 475111 and approved by Sarasin Asset Management Limited (“SAM”), a limited liability company registered in England and Wales with company registration number 01497670, which is authorised and regulated by the UK Financial Conduct Authority with firm reference number 163584 and registered as an Investment Adviser with the US Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. The information in this document has not been approved or verified by the SEC or by any state securities authority. Registration with the SEC does not imply a certain level of skill or training.

In rendering investment advisory services, SAM may use the resources of its affiliate, S&P, an SEC Exempt Reporting Adviser. S&P is a London-based specialist investment manager. SAM has entered into a Memorandum of Understanding (“MOU”) with S&P to provide advisory resources to clients of SAM. To the extent that S&P provides advisory services in relation to any US clients of SAM pursuant to the MOU, S&P will be subject to the supervision of SAM. S&P and any of its respective employees who provide services to clients of SAM are considered under the MOU to be “associated persons” as defined in the Investment Advisers Act of 1940. S&P manages mutual funds in which SAM may invest its clients’ assets as appropriate. To the extent that SAM is able to exercise proxy voting on behalf of its clients, SAM follows the policy set by S&P. Proxy voting is an operational process dependent upon support from SAM’s clients’ custodians, some of which do not support proxy voting in all or certain markets.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance. Management fees and expenses are described in SAM’s Form ADV, which is available upon request or at the SEC’s public disclosure website, https://www.adviserinfo.sec.gov/Firm/115788.