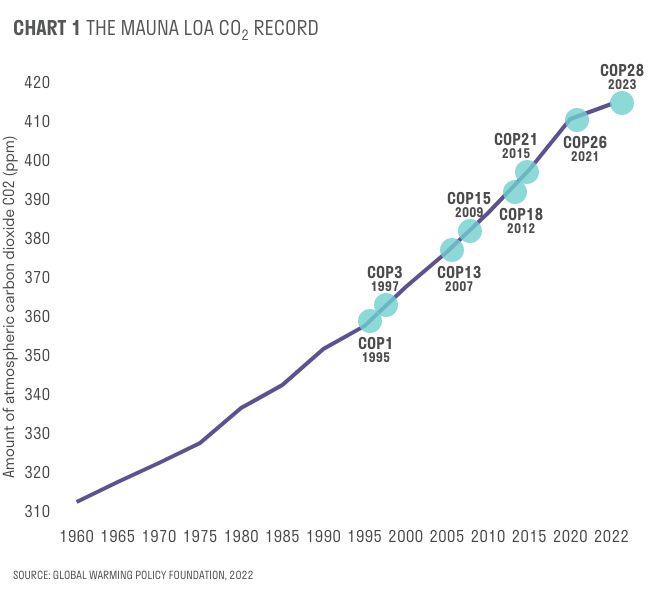

Let’s face it. Despite world leaders putting on a brave face at the latest round of international climate negotiations – the 28th Conference of Parties (COP28) – the headline result fell dangerously short of what is required. It speaks volumes that this was the first COP to acknowledge that decarbonisation would require a transition away from fossil fuels.

The question for investors, and indeed society, is whether another failed COP matters.

Clean tech accelerates

Our answer is: yes, it matters. The energy transition will be easier and faster with concerted governmental support. But we mustn’t allow the gloom of policy paralysis to blind us to the accelerating clean tech revolution.

In the International Energy Agency’s (IEA) June 2023 Renewable Energy Market Update, the evidence of transition is clear.1 Global additions of renewable power capacity are expected to jump by a third in 2023, the largest absolute increase ever, to more than 440 gigawatts. Solar is the stand-out performer, with manufacturing capacity on track to meet the level of demand envisaged in the IEA’s Net Zero Emissions by 2050 scenario.

Rather than slowing down the transition, the Ukraine-Russia conflict has led to acceleration. The forecast for renewable capacity additions in Europe has been revised upwards by 40%.

Cheaper than fossil fuels

Critically, far from imposing costs on consumers, the IEA estimates that wholesale electricity prices in Europe would have been 8% higher in 2022 without the additional renewable capacity.[1] Clean energy will continue to take market share for the simple reasons that it is already – or rapidly becoming – cheaper, more accessible and less vulnerable to geopolitical ructions than fossil fuels.

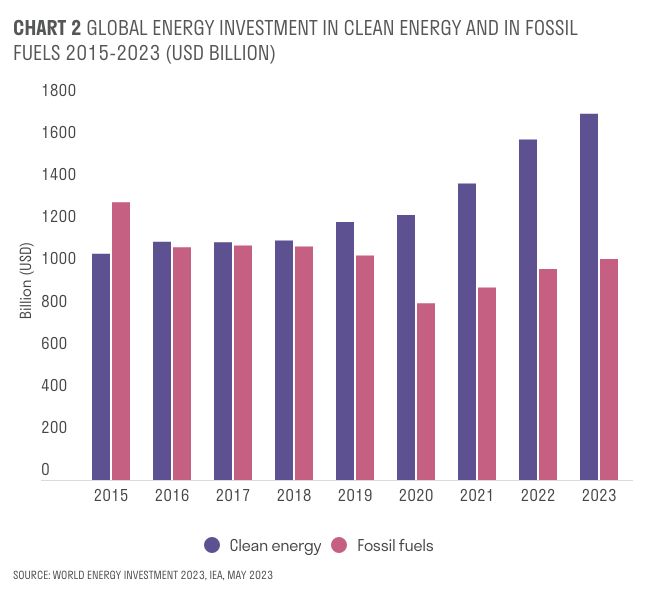

The attractions of clean energy over fossil fuels is clear from the massive shift in financing, as shown in chart 2.[2] For every $1 spent on fossil fuels today, $1.7 is spent on clean energy. Five years ago, this ratio was 1:1. In the electricity market alone, low-emissions power is expected to account for almost 90% of total investment in generation for 2023.

Can the market keep us within 1.5°C?

The market forces behind clean tech are powerful, but are they enough to keep temperature increases to a 1.5°C limit? While we can’t know for sure, the IEA’s scenario analysis points to a shortfall. The Stated Policies scenario (STEPS) shows where the IEA expects us to be by 2030 given current policies. Even under the Announced Pledges Scenario (APS), which includes commitments for new policies, we are falling short of what is needed in a 1.5°C scenario targeting net zero emissions by 2030.

While the economics are powerful, the mountain we have to climb to get to net zero is gargantuan. We need everyone, including governments, pulling in the same direction. Above all, governments need to stop obstructing progress. By continuing to subsidise harmful fossil fuel consumption, failing to reform permitting rules for energy and underinvestment in infrastructure for a new age of green technologies, governments add to the obstacles to transition.

So, the COP process does matter and is failing to deliver. However, if we look more closely there is a perceptible silver lining from the latest negotiations. Given the meeting was hosted by a petrostate, it is arguably remarkable that any progress was made. The COP28 President, Sultan Al Jaber (also chair of Abu Dhabi National Oil Company), stood firm behind the need to “keep the 1.5°C North Star alive”.

More steps forward than back

The IEA estimates that the new commitments on methane leakage in oil and gas production, increasing renewables, carbon capture and storage, as well as energy efficiency, will deliver 30% of what is needed for a 1.5°C outcome. While not a major leap forward, it was not a reversal either.

Change rarely happens in a linear fashion. The clean tech revolution, which is already demonstrating its ability to surprise repeatedly on the upside, is no different.

Those with vested interests in the fossil fuel economy will inevitably resist. But in this transition, it is increasingly clear that the most powerful force for change – the market – is moving behind a sustainable planet. This is not just a human imperative; it is also increasingly an economic reality that our clients can benefit from.

[1] Renewable energy market update, IEA, June 2023

[2] World Energy Investment 2023, IEA, May 2023

Important information

This document is intended for retail investors. You should not act or rely on this document but should contact your professional adviser.

This document has been issued by Sarasin & Partners LLP of Juxon House, 100 St Paul’s Churchyard, London, EC4M 8BU, a limited liability partnership registered in England and Wales with registered number OC329859, and which is authorised and regulated by the Financial Conduct Authority with firm reference number 475111.

This document has been prepared for marketing and information purposes only and is not a solicitation, or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2024 Sarasin & Partners LLP – all rights reserved. This document can only be distributed or reproduced with permission from Sarasin & Partners LLP. Please contact marketing@sarasin.co.uk.