The Prime Minister’s resignation, taken in isolation, has been digested calmly by markets. This is largely because markets had anticipated the resignation and yields have been increasing over recent months to reflect the associated risks.

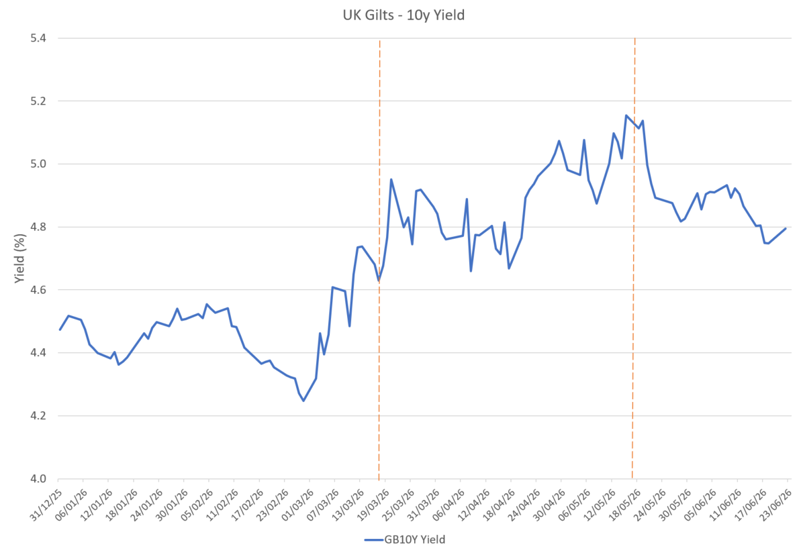

You can see from the below chart that UK borrowing costs (as represented by the UK 10-year government bond yield) have increased from a little over 4% to 4.8% today; having peaked at over 5% (with longer-dated parts of the UK government bond market reaching levels not seen since 1998 in May). A significant proportion of this increase has been the result of higher global inflation expectations following the Iran War, with markets adjusting to reflect expectations of higher interest rates in response. Nevertheless, there has undoubtedly been additional pressure here in the UK as a result of the political uncertainty surrounding Keir Starmer’s resignation and, more importantly, the potential choice of Chancellor and approach to government spending and borrowing that may follow.

Source: Factset

In anticipation of the event, we have recalibrated our modelling of fair values for the UK 10-year government bond yield. We focused on the negative reaction to the Liz Truss mini-Budget of 2022 as a reasonable recent stress test and have concluded that even under a more severe scenario such as this, where the incoming Prime Minister and new Chancellor abandon Reeves’ fiscal rules and announce a significant spending package, current yields above 4.8% still represent good long-term value. Accordingly, we have twice topped up our UK government bond holdings when the UK 10-year yield approached or exceeded 5%, as shown above.

We are, of course, continuing to monitor the situation very closely, and have the tools to act quickly should the evidence on the ground changes. For the time being though we believe that uncertainty has created a window of opportunity and we have sought to take advantage of it for clients.

Important Information

This video is intended for retail investors and/or private clients. You should not act or rely on any information contained in this document without seeking advice from a professional adviser.

This is a marketing communication. Issued by Sarasin & Partners LLP, 50 George St, London, W1U 7DY. Registered in England and Wales, No. OC329859. Authorised and regulated by the Financial Conduct Authority (FRN: 475111). Website: www.sarasinandpartners.com. Tel: +44 (0)20 7038 7000. Telephone calls may be recorded or monitored in accordance with applicable laws.

This document has been produced for marketing and informational purposes only. It is not a solicitation or an offer to buy or sell any security. The information on which the material is based has been obtained in good faith, from sources that we believe to be reliable, but we have not independently verified such information and we make no representation or warranty, express or implied, as to its accuracy. All expressions of opinion are subject to change without notice.

This document should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this material when taking individual investment and/or strategic decisions.

Capital at risk. The value of investments and any income derived from them can fall as well as rise and investors may not get back the amount originally invested. If investing in foreign currencies, the return in the investor’s reference currency may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results and may not be repeated. Forecasts are not a reliable indicator of future performance. The index data referenced is the property of third-party providers and has been licensed for use by us. Our Third-Party Suppliers accept no liability in connection with its use. See our website for a full copy of the index disclaimers https://sarasinandpartners.com/important-information/.

Neither Sarasin & Partners LLP nor any other member of the J. Safra Sarasin Holding Ltd group accepts any liability or responsibility whatsoever for any consequential loss of any kind arising out of the use of this document or any part of its contents. The use of this document should not be regarded as a substitute for the exercise by the recipient of their own judgement. Sarasin & Partners LLP and/or any person connected with it may act upon or make use of the material referred to herein and/or any of the information upon which it is based, prior to publication of this document.

Where the data in this document comes partially from third-party sources the accuracy, completeness or correctness of the information contained in this publication is not guaranteed, and third-party data is provided without any warranties of any kind. Sarasin & Partners LLP shall have no liability in connection with third-party data.

© 2026 Sarasin & Partners LLP. All rights reserved. This document is subject to copyright and can only be reproduced or distributed with permission from Sarasin & Partners LLP. Any unauthorised use is strictly prohibited.